numpy.corrcoef¶

- numpy.corrcoef(x, y=None, rowvar=1, bias=0)¶

Return correlation coefficients.

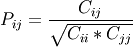

Please refer to the documentation for cov for more detail. The relationship between the correlation coefficient matrix, P, and the covariance matrix, C, is

The values of P are between -1 and 1.

See also

- cov

- Covariance matrix