scipy.stats.rv_discrete¶

- class scipy.stats.rv_discrete(a=0, b=inf, name=None, badvalue=None, moment_tol=1e-08, values=None, inc=1, longname=None, shapes=None, extradoc=None)[source]¶

A generic discrete random variable class meant for subclassing.

rv_discrete is a base class to construct specific distribution classes and instances from for discrete random variables. rv_discrete can be used to construct an arbitrary distribution with defined by a list of support points and the corresponding probabilities.

Parameters: a : float, optional

Lower bound of the support of the distribution, default: 0

b : float, optional

Upper bound of the support of the distribution, default: plus infinity

moment_tol : float, optional

The tolerance for the generic calculation of moments

values : tuple of two array_like

(xk, pk) where xk are points (integers) with positive probability pk with sum(pk) = 1

inc : integer

increment for the support of the distribution, default: 1 other values have not been tested

badvalue : object, optional

The value in (masked) arrays that indicates a value that should be ignored.

name : str, optional

The name of the instance. This string is used to construct the default example for distributions.

longname : str, optional

This string is used as part of the first line of the docstring returned when a subclass has no docstring of its own. Note: longname exists for backwards compatibility, do not use for new subclasses.

shapes : str, optional

The shape of the distribution. For example "m, n" for a distribution that takes two integers as the first two arguments for all its methods.

extradoc : str, optional

This string is used as the last part of the docstring returned when a subclass has no docstring of its own. Note: extradoc exists for backwards compatibility, do not use for new subclasses.

Notes

You can construct an arbitrary discrete rv where P{X=xk} = pk by passing to the rv_discrete initialization method (through the values=keyword) a tuple of sequences (xk, pk) which describes only those values of X (xk) that occur with nonzero probability (pk).

To create a new discrete distribution, we would do the following:

class poisson_gen(rv_discrete): # "Poisson distribution" def _pmf(self, k, mu): ...

and create an instance:

poisson = poisson_gen(name="poisson", longname='A Poisson')

The docstring can be created from a template.

Alternatively, the object may be called (as a function) to fix the shape and location parameters returning a “frozen” discrete RV object:

myrv = generic(<shape(s)>, loc=0) - frozen RV object with the same methods but holding the given shape and location fixed.A note on shapes: subclasses need not specify them explicitly. In this case, the shapes will be automatically deduced from the signatures of the overridden methods. If, for some reason, you prefer to avoid relying on introspection, you can specify shapes explicitly as an argument to the instance constructor.

Examples

Custom made discrete distribution:

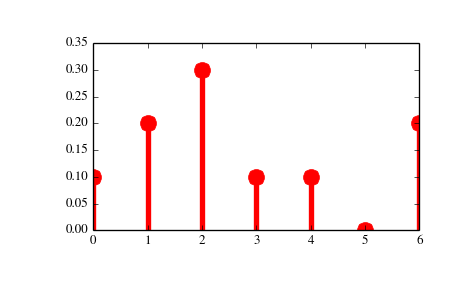

>>> from scipy import stats >>> xk = np.arange(7) >>> pk = (0.1, 0.2, 0.3, 0.1, 0.1, 0.0, 0.2) >>> custm = stats.rv_discrete(name='custm', values=(xk, pk)) >>> >>> import matplotlib.pyplot as plt >>> fig, ax = plt.subplots(1, 1) >>> ax.plot(xk, custm.pmf(xk), 'ro', ms=12, mec='r') >>> ax.vlines(xk, 0, custm.pmf(xk), colors='r', lw=4) >>> plt.show()

Random number generation:

>>> R = custm.rvs(size=100)

Methods

generic.rvs(<shape(s)>, loc=0, size=1) random variates generic.pmf(x, <shape(s)>, loc=0) probability mass function logpmf(x, <shape(s)>, loc=0) log of the probability density function generic.cdf(x, <shape(s)>, loc=0) cumulative density function generic.logcdf(x, <shape(s)>, loc=0) log of the cumulative density function generic.sf(x, <shape(s)>, loc=0) survival function (1-cdf — sometimes more accurate) generic.logsf(x, <shape(s)>, loc=0, scale=1) log of the survival function generic.ppf(q, <shape(s)>, loc=0) percent point function (inverse of cdf — percentiles) generic.isf(q, <shape(s)>, loc=0) inverse survival function (inverse of sf) generic.moment(n, <shape(s)>, loc=0) non-central n-th moment of the distribution. May not work for array arguments. generic.stats(<shape(s)>, loc=0, moments='mv') mean(‘m’, axis=0), variance(‘v’), skew(‘s’), and/or kurtosis(‘k’) generic.entropy(<shape(s)>, loc=0) entropy of the RV generic.expect(func=None, args=(), loc=0, lb=None, ub=None, conditional=False) Expected value of a function with respect to the distribution. Additional kwd arguments passed to integrate.quad generic.median(<shape(s)>, loc=0) Median of the distribution. generic.mean(<shape(s)>, loc=0) Mean of the distribution. generic.std(<shape(s)>, loc=0) Standard deviation of the distribution. generic.var(<shape(s)>, loc=0) Variance of the distribution. generic.interval(alpha, <shape(s)>, loc=0) Interval that with alpha percent probability contains a random realization of this distribution. generic(<shape(s)>, loc=0) calling a distribution instance returns a frozen distribution