numpy.corrcoef¶

- numpy.corrcoef(x, y=None, rowvar=1, bias=0)¶

Return correlation coefficients.

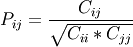

Please refer to the documentation for cov for more detail. The relationship between the correlation coefficient matrix, P, and the covariance matrix, C, is

The values of P are between -1 and 1.

Parameters: m : array_like

A 1-D or 2-D array containing multiple variables and observations. Each row of m represents a variable, and each column a single observation of all those variables. Also see rowvar below.

y : array_like, optional

An additional set of variables and observations. y has the same shape as m.

rowvar : int, optional

If rowvar is non-zero (default), then each row represents a variable, with observations in the columns. Otherwise, the relationship is transposed: each column represents a variable, while the rows contain observations.

bias : int, optional

Default normalization is by (N-1), where N is the number of observations given (unbiased estimate). If bias is 1, then normalization is by N.

Returns: out : ndarray

The correlation coefficient matrix of the variables.

See also

- cov

- Covariance matrix